Making state-owned banks viable, allowing them to charge fees for services to the government

Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

The private sector has been exploring in recent months overseas funds at competitive rates but at low cost. These funds are available at LIBOR plus a minimal rate of interest. Despite vulnerability to currency fluctuation, our private sector has started accessing these sources of finance at large. Many more good and prudent entrepreneurs are shifting to these cheaper sources from high rate of two-digit local bank finances. Only bad non-performing loan (NPL) holders, who are addicted to re-scheduling and rephasing culture of loans at the behest of the government, the Board of Directors and bureaucratic influence in state-owned commercial banks (SoCBs) will eventually be SoCB clients. More so because of non-commercial attitudes of SoCB management, these loanees are shifting to cheaper overseas sources. As a result, state-owned commercial banks will face more dire business consequences in banking than ever before.

Time is now ripe for the SoCBs to regularise NPLs. In this regard, the government must form a task force or NPL Commission to be adequately empowered to deal with NPL intricacies professionally. Also in place of capital injections through budget allocation, the government should pay charges to SoCBs for services obtained from them. Also the Treasury Bills and Bonds must be at a rate of interest covering cost of fund. The NPLs must be reduced to come to less than 3 per cent in 5 years' crash programme. The Task Force or NPL Commission must be manned by professionally sound, dedicated and honest persons. It must be duly empowered with bureaucratic control and intervention. Its accountability has be made to the Public Accounts Committee (PAC) and the Jatiya Sangsad through Bangladesh Bank. The observations and findings of NPL Commission or for that matter, Task Force will come up for consideration after holding symposiums and workshops.

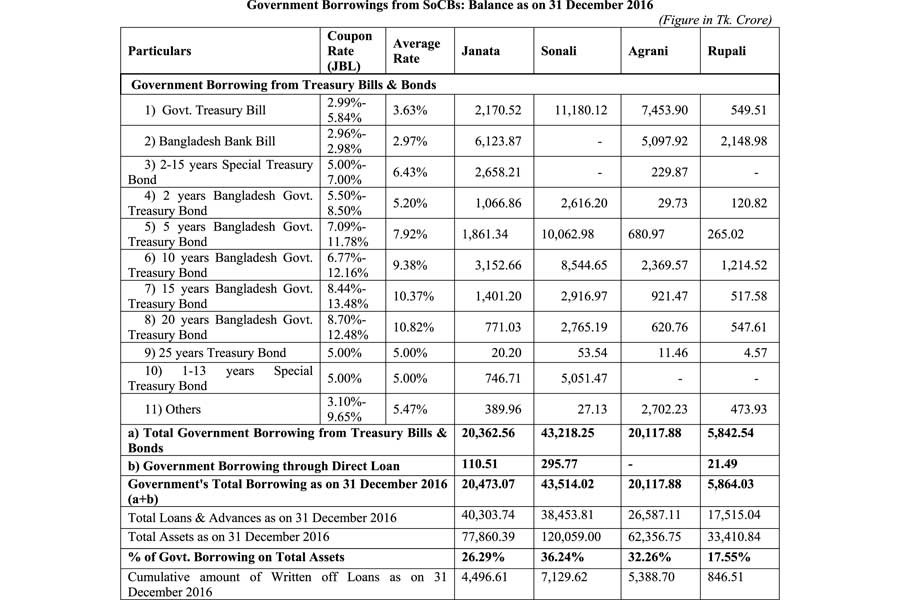

Latest Bangladesh Bank data showed that the banks faced a capital shortfall of Tk. 176.25 billion as of September this year, up by over Tk 50 billion a quarter ago:

Huge deposits are now lying idle with SoCBs involving cost of fund. The average cost is 8 per cent or above. This cost stems from huge sum of NPLs burdened on those banks. On an average, 25 per cent to 40 per cent of NPLs are currently burdened on them. Taking the year-end restructuring and rephasing out of books, this figure would be higher. The top 20 defaulters are said to have formed powerful cartel. These defaulters, almost all being willful having connivance with the lending management, are omni-powerful to control even many strategic government decisions. The appointments of SoCB top-notch bankers are held at their behest. The lendings are never assessed on the basis of feasibility and market perspectives.

Many assessed valuations of assets and properties are biasedly made only to offer higher loan amounts to clients. The debt servicing through cash generation from projects lent by banks is seldom considered. Even during project period restructuring, applications are largely received by SoCBs. Also increased amounts of lending are requested for. Again access to courts by clients aggravates the situation. Many verdicts favouring the clients have rendered the banks' loaned funds at risk.

SoCBs manage collection of foreign remittance inward for the government. Tk. 10 account opening for farmers, payment services of allowances for freedom fighters, destitute, elderly people and widows are all done free of charge from these banks. Collection of fees for admission to schools and rendering banking services to many are also made by SoCBs free of charge. In a large number of government social safety network programmes, payments of funds are conducted by SoCBs again free of cost. Not even a modest commission is charged. But on the contrary, banking personnel are actively involved in all these services. The cost of fund is 80 per cent now mainly burdened by NPLs. This is more a burden as SoCBs have to invest mandatorily in government bonds and Bangladesh Bank bills etc at interest rates much lower than cost of fund invested.

All the state-owned commercial banks in Bangladesh carry out government banking services. Many of these have become the highest taxpayers and achieved the highest profit. Besides performing its general banking services, the banks participate in the safety-net programmes of the government. The functions of SoCBs are not comparable to those of the private commercial banks even though in some indicators, SoCBs are marching ahead. If costs of rendering services to these fields are expressed in terms of money, the actual contribution of the banks to the nation will be much higher than those in our accounts. The safety-net programmes' financial value will be much more than last budget capital injection of Tk. 20 billion for these SoCBs.

The Sonali Bank also works for government treasury functions.

Besides the programmes cited above, different types of telephone, gas, municipal tax, electricity bills are collected by the banks on behalf of the government. Primary student stipends, retirement allowance for government service holders, savings certificate, army pension etc. are also disbursed. All these services are free of cost. As such the value of these services can be considered as receivable for SoCBs from the government. The terminology of 'capital injections' can be replaced by government services cost to SoCBs.

The subsidies to state-owned enterprises (SoEs) from SoCBs, which are eventually bad loans should be stopped. Or at least cost of servicing these loans should be paid by the government to these state banks. At the end, SoCBs are not really a liability but a bare necessity to the government. Indeed, these services derived by the government are not available from private commercial banks (PCBs).But then open ends to SoCBs cannot be allowed to continue unabated. Because it is the depositors' money involved, not of any others. So it is better that these banks are more regulated competitively and professionally by Bangladesh Bank without any bias. However, dual regulation over these will jeopardise better prospects for these banks.The capital injection can be replaced as fees for such services rather than alms often blaming inefficient SoCBs. Huge branch networks should also be business and need- based. These networks need to be rationalised.

Masih Malik Chowdhury, FCS FCA, is Founder

Partner MasihMuhithHaque&Co,

Chartered Accountants & Past President ICAB.