Published :

Updated :

For all latest news, follow The Financial Express Google News channel.

For all latest news, follow The Financial Express Google News channel.

With Covid-19 completely dismantling the economy, innovation sprung in different spheres of business as coping mechanisms. With regard to international business, trade finance –constituting financial product and solutions that facilitate cross-border transactions under regulatory surveillance – also received few updates. Existing trade finance regulatory provisions and banking practices in Bangladesh required restructuring for a while now; its significance was genuinely felt during the pandemicsince March 2020. Hence, several digitisation initiatives are required, mobilised by regulatory support and the introduction of Blockchain technology, to kick-start the next generation of trade finance.

The volume of international business is reflected by $35 billion exports and $56 billion imports during FY 2018-19 according to Bangladesh Bank. During each LC opening which is the prerequisite for each cross-border transaction, our regulation requires submitting several hardcopies e.g. insurance cover notes and Letter of Credit Authorisation Forms (LCAF) for import LCs. Extensive time is consumed in collecting hardcopy authorisation and commute to complete the process. With the country under lockdown, the emergence of work from home (WFH) and limited banking operation during April and May, it became highly challenging for businesses to fulfil these requirements. The situation started normalising since June with offices and regular banking operation gradually resuming. Resultantly, Covid cases among employees surged. The future seems bleak with winter knocking and a second wave is predicted,and things are not looking optimistic globally. If the prediction is right, another lockdown and subsequent limited banking operation are highly likely, bringing us back to the same old woes. Therefore, before things get worse, it is high time banks, leading corporates and regulators come forward to digitise relevant hardcopy requirements while ensuring security against financial fraud.

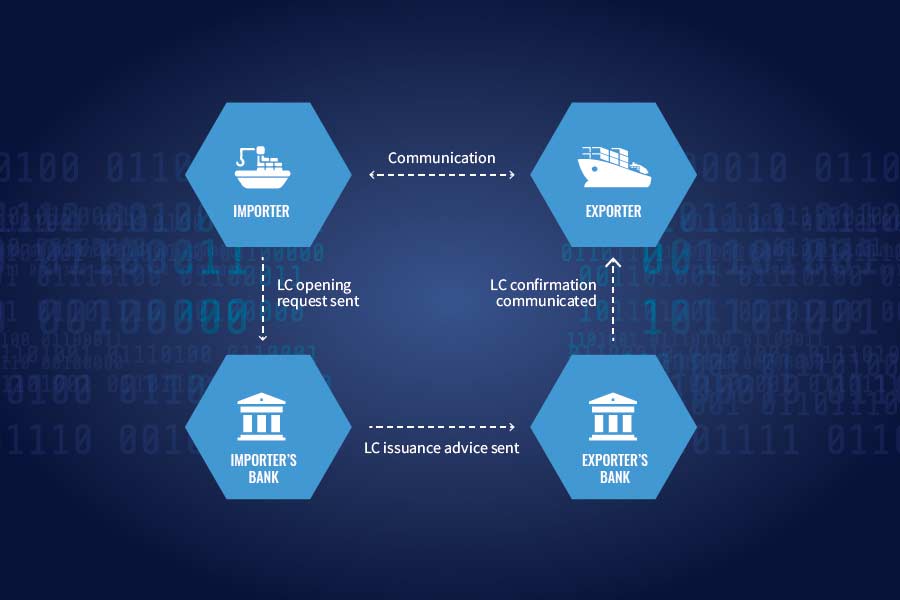

Along this way, the next-gen Bangladesh trade finance might start by implementing Blockchain for LC opening and settlement. It involves creating a network of participating importers, exporters, and their corresponding banks. Using the platform, the importer and exporter can communicate with each other and share the draft LC before finalising it. After it is checked by both parties, it flows to the LC issuing bank i.e. importer’s bank for issuance. The issuing bank can then send the LC advice to the beneficiary bank i.e. exporter’s bank all while using the platform instead of sending SWIFT message. This allows the beneficiary bank to receive LC advise in real-time for confirmation.

(Figure: LC issuance process using the Blockchain platform)

As explained in the figure, the entire communication happens across parties using Blockchain platform in real-time. Conventional LC opening process involves multiple steps and persistence to ensure timely communication; thus,it is prone to discrepancies. Since the entire process does not require any hardcopy documentation, the role of regulation will be critical in implementing the solution in a scalable manner. The possibility of Blockchain can also be extended to shipping document retirement by bringing shipping line companies to the network to introduce the electronic bill of lading.

On a brighter note, banks are rolling out their online trade platforms to expedite the digital movement. The platforms are designed to replace hardcopy instructions and requests not mandated by regulation e.g. LCA forwarding letter, document acceptance and shipping guarantee issuance. Since these initiatives are supposed to change the existing way of working, it requires top management support of businesses to incorporate the new culture. From the bank’s perspective, it must be ensured that the platforms are constructed in a user-friendly way.

To conclude, with the second and probably the third wave of Covid-19 predicted around the world, it is safe to assume that work from home will prevail till a recognised vaccine is found. Regardless, the post-covid workplace will include more virtual activity as the potential of running giant companies through technology is demonstrated in these trying times. All these underpin the digital movement happening unfolding and their unbound possibilities. However, banks should have a serious commitment toward customer data protection and their responsible usage. We have seen reports in the past where online banking accounts were compromised by unauthorised access, causing customers financial loss and banks their reputation. Several layers of proactive, maintenance and reactive IT measures would save banks from such incidents and boost customer confidence in adopting digital means.

The writer is a treasury professional at a multinational fast-moving consumer goods company who can be reached at wahidulislam041@gmail.com