Financial inclusion can be simply defined as the universal access to and use of affordable, quality financial services, provided responsibly. The goal of financial inclusion is to bring the financially-excluded under the umbrella of formal financial services, so as to protect and enhance welfare. Formal financial inclusion entails access to credit, savings products, micro-insurance and payments. There are various beneficial outcomes to financial inclusion.

An important corollary to the discussion on financial inclusion is the topic of financial literacy. It has been posited that financial exclusion is often involuntary, and can take place because of lack of financial literacy, e.g., perceived barriers in the minds of the underserved. Other scholars have also emphasised the importance of financial literacy, referring to financial awareness, knowledge of banks and banking channels, as well as available financial products. This report does not delve into particularities of financial literacy in Bangladesh, formal and informal mechanisms that exist, or the scope for such. Nevertheless, this is an area that requires attention of researchers and policy intervention.

Current State of Financial Inclusion: After decades of microfinance, its various achievements and criticisms notwithstanding, we have clear evidence that there is demand for financial services among the underserved. While microfinance institutions constituted the drivers of financial inclusion in the past, it is evident that the ecosystem will be more complex and digitally oriented, in the future. Until now, most bank branches (or ATMs) are concentrated in urban areas, and high costs of setting up bank branches in rural areas have dissuaded banks from reaching the last-mile customer. However, digital financial services (DFS), which are currently almost exclusively, bank-owned and bank-run, will allow banks to reach the last-mile customer. The newest entrants in the DFS space, with the widest potential for mass market penetration, are mobile financial services (MFS) and agent banking services.

Mobile Financial Services: McKinsey, the world's leading management consulting company, considers MFS to be the most effective conduit to reach the unbanked. Mobile phone penetration, which stood at 80 percent in emerging markets in 2014, is expected to increase to 90 percent by 2020, according to GSMA data. In Bangladesh, MFS has also had a noteworthy journey of growth thus far. Starting in 2011, with the establishment of a BRAC Bank subsidiary named bKash, a total of 18 banks are currently providing MFS services in Bangladesh while 28 are licensed to do so. BRAC Bank's "bKash" and Dutch Bangla Bank's "Rocket" are the leading players, although bKash accounts for more than 80% of total MFS transactions.

Highlights of MFS in Bangladesh

Source: Bangladesh Bank

The successes of MFS in Bangladesh and of bKash in particular have generated global attention, much like the case for Kenya and M-PESA. Bangladesh's high mobile phone penetration (120.73 million) and low banking sector penetration (50 million) created the persuasive argument for DFSin order to close the inclusion gap. According to the Bangladesh Bank, as of August 2017, the average value of transactions per day reached BDT 1,038 crore or US$ 130 million as in the figure above.

However, MFS in Bangladesh is yet to become a conduit for formal banking products such as savings and credit products. Most of the users use it for payments-related services. Cash-in and cash-out transactions are dominant, followed by P2P transactions.

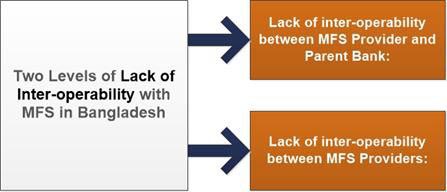

Bangladesh Bank guidelines have thus far allowed only a bank-led model to provide MFS services. The idea is that a customer's mobile account will rest with a bank and he or she will be able to access this account through a mobile device. However, a complete integration between a parent bank's services and the mobile wallet is yet to take place. This is a case of lack of interoperability. In fact, the MFS sector is still hindered by two levels of lack of interoperability (See the figure on Lack of Interoperability).

Lack of Interoperability in MFS

Agent Banking Ecosystem

While MFS is yet to become an extension of banks in the sense of providing banking services such as credit and savings products to users, its success lies in the exponential growth in the number of transactions conducted on it daily, highlighting a similar growth in people's trust in the digital platform. It is expected that as more and more users open mobile wallets, and existing users use their wallets more frequently, the business case for offering banking products and services digitally at the retail level to the under-served, will be inevitable. Until that happens, agent banking, the other much talked-about bank-led DFS innovation has the potential to fill this gap, as banks try to look for newer customers among the under-served, and policy makers attempt to actualize further financial inclusion.

Agent Banking: Officially sanctioned by the Bangladesh Bank in 2013, agent banking has only recently begun to take off. It is considered to be the latest innovation in banking services and is persuading banks to think beyond CSR and focus on business imperatives with a view towards serving the unbanked.

The ecosystem for agent banking, as it stands, can also be represented through a doughnut of actors and rules (See the figure on Agent Banking Ecosystem). Banks, once again, are the key driver for agent banking, since they are the only licensed entities that can offer this service. Multilaterals have played a salient role in driving agent banking such as United Nations Capital Development Fund (UNCDF). The Rural Electrification Board (REB) has also provided agents with a source of additional income as Bangladesh Bank now allows people to pay their utility bills to REB through agent banking agents.

Technology providers are key, be it providers of hardware at agent points or software at either the agent or the bank's end, not to mention services that aim to integrate customer information across the service delivery chain. International NGOs (INGOs) have played a key role in the early stage of agent banking, since they possess considerable expertise in developing products for and marketing to the underserved. INGOs refer to the building of such awareness as "behavioral change communication." Such communication will be essential in generating financial literacy among the underserved and bringing them into the fold of formal banking services, through agent banking. According to Bangladesh Bank guidelines, microfinance institutions will not be left behind as banks gear up to serve the last mile, because they will be eligible to service banks as agents. In fact, it is believed that microfinance institutions may play a key role in connecting banks to the underserved given their long experience in developing products and servicing them.

However, at this early stage of agent banking's development, there remain significant constraints. Although officially allowed by the Bangladesh Bank since 2013, it was not until 2015-16, that the leading players in this market, e.g. Dutch-Bangla Bank and Bank Asia, began to scale operations. Consequently, there are certain preliminary constraints and bottle-necks (See the figure on Constraints in Agent Banking System). The Bangladesh Bank, as per the Prudential Guidelines announced in September 2017, has addressed some of these constraints, such as providing clarification regarding roles of agents, oversight by banks; liquidity management by agents; as well as financial literacy requirements for agents, bankers, and customers.

Among the constraints identified, the lack of a clear definition of "agent" translated to various entities, individuals and institutions, have tried their hands at serving as banking agents, with patchy success. With formalization of the definition, the market will be better served by agents with the appropriate credentials. A related problem is that agents have often lacked sufficient financial incentive to dedicate all his or her resources to banking operations. Often, these agents have cross-subsidized their agent banking businesses with others, such as airtime top-up or even other forms of retail. A recent provision allowing agent banking agents to collect utility bills for the REB addresses the problem of financial incentive, to some extent. Other problems include a hesitation of female customer to interact with male agents. This can be addressed with increasing the number of female agents that can service particular female segments initially, for example RMG workers, and to larger female populations, subsequently.

Banks should also look to afford the same level of seriousness to their agent banking operations that they would, to other more mainstream banking services. For instance, interviews conducted with banks suggest that certain banks housed their agent banking operations under other departments, often arbitrarily (e.g. in cards or even IT). Overtime, banks are expected to realize the business value propositions of agent banking, and stop seeing it as either ornamental or as CSR initiative. This will also accelerate the time taken to get agent banking products approved by the boards. And last but not least, it is salient that financial literacy sessions and financial counseling ought to be provided at agent points, indicating that banks ought to also invest in training-of-trainers (ToT) and related activities. Encouragingly, the Bangladesh Bank has taken notice of this and encouraged banks to do the same.

Policy Recommendations: In the course of research for this report, which included interviews with key informants such as bank sector, multilateral donor and INGO officials, it is evident that despite recent successes, the private and public sector have some ways to go to actualize the potential for financial inclusion in Bangladesh.

With regard to the private sector, if one considers agent banking, it is evident that not all participating banks have a coherent strategy and business model with which to target segments of the under-banked market. Banks can capitalize on investments already made, even if they have been made by non-banking entities, such as International NGOs (INGOs) and other potential development sector partners, which tend to be better at understanding this segment of the market. A few banks have already begun to partner with INGOs to better understand how to approach this market.

Banks with agent banking licenses must carefully consider the early-mover advantages to the business of financial inclusion and devise governance processes in line with coherent corporate strategies. These strategies should encourage short-term investments in view of long-term returns, both in terms of profitability and branding value propositions. Capacity building is another important area, as banks need to build capacity to recruit, train, and manage agent banking networks, respecting both the uniqueness of agent banking operations relative to existing banking products, while not rendering them too exceptional to be integrated into strategic priorities.

The government of Bangladesh, through various ministries, departments and initiatives, has taken cognizance of the importance of and potential for financial inclusion and DFS, respectively. Salient are the role of the Bangladesh Bank and the Access to Information (A2i) initiative. The latter has sought to create Union Digital Centers (UDCs) to serve as agent banking points. The MRA and Palli Karma-Sahayak Foundation (PKSF) have also worked closely with international partners and multilaterals to refresh their thinking on financial inclusion.

As next steps, it is important for the government to set specific, measurable targets related to accomplishments in financial inclusion in line with global standards followed by the Alliance for Financial Inclusion as part of their Maya Declaration targets. Consumer protection has recently been announced through the September 2017 Prudential Guidelines. However, this remains an area where coordination with financial services providers and civil society entities remain important, so that customers of agent banking and mobile financial services are aware of the redress mechanisms and protection facilities.

Financial technology, or Fintech, as it is widely known, will also be a clear driver and catalyst for DFS-led financial inclusion. There remain several opportunities for the public and private sector to maximize the benefits and mitigate risks associated with Fintech. Fintech will entail integration of legacy systems in banks with IT systems required for MFS and agent banking. This is likely to be time-consuming and fraught with near-term challenges that bank boards need to embrace. Fintech entities, start-ups or more established companies, should also welcomeand if necessary, make the case for "regulatory sandboxes" in which to operate within prescribed timelines to showcase the utility of their innovation (Brookings, 2017). The central bank should also mandate that Fintech companies be subject to cyber-security assessments and risk management trainings.

Last but not least, a much-needed Fintech-related innovation that is hopefully forthcoming is electronic KYC, or e-KYC. The UNCDF's Shift Project identifies e-KYC and "tiered KYC" as one of the salient challenges to including the under-banked. Existing KYC procedures constitute a significant barrier to formal financial inclusion. The database of National Identity (NID) that the Bangladesh Election Commission (BEC) has been developing, can facilitate the introduction e-KYC by financial services providers, and drive DFS adoption and financial inclusion. The UNCDF in Bangladesh prescribes a set of steps (See the figure on Steps towards E-KYC and Tiered KYC) in order to actualise e-KYC and tiered KYC. As is evident, improved coordination between firstly regulators, subsequently private sector players in harmonizing KYC can lead to development of practical guidelines on e-KYC and tiered KYC, which can remove a significant barrier to adoption of DFS.

Constraints in the Agent Banking System

Steps towards E-KYC and Tiered KYC

Source: Drafted by Author based on UNCDF Concept Note

This piece is intended to contribute to the sectoral and policy knowledge that can inform and guide debates on digital financial services (DFS) and financial inclusion. While DFS is not the exclusive path to financial inclusion, it is evident that is likely to become the most enduring and effective path, until the mobile phone becomes the euphemistic mattress under which Bangladeshis store their hard-earned income.

The writer is director of the Centre for Enterprise and Society.

Email:sajid.amit@ulab.edu.bd